An accident settlement loan, also known as pre-settlement funding, can be a vital lifeline for individuals involved in personal injury claims, including car accidents, workplace injuries, and more. If you live in Florida and are involved in a personal injury lawsuit, you might be facing financial stress while waiting for your settlement. This guide will walk you through everything you need to know about securing an accident settlement loan in Florida—how it works, who qualifies, what it costs, and how to compare funding providers.

2. What Is an Accident Settlement Loan (Pre-Settlement Funding)?

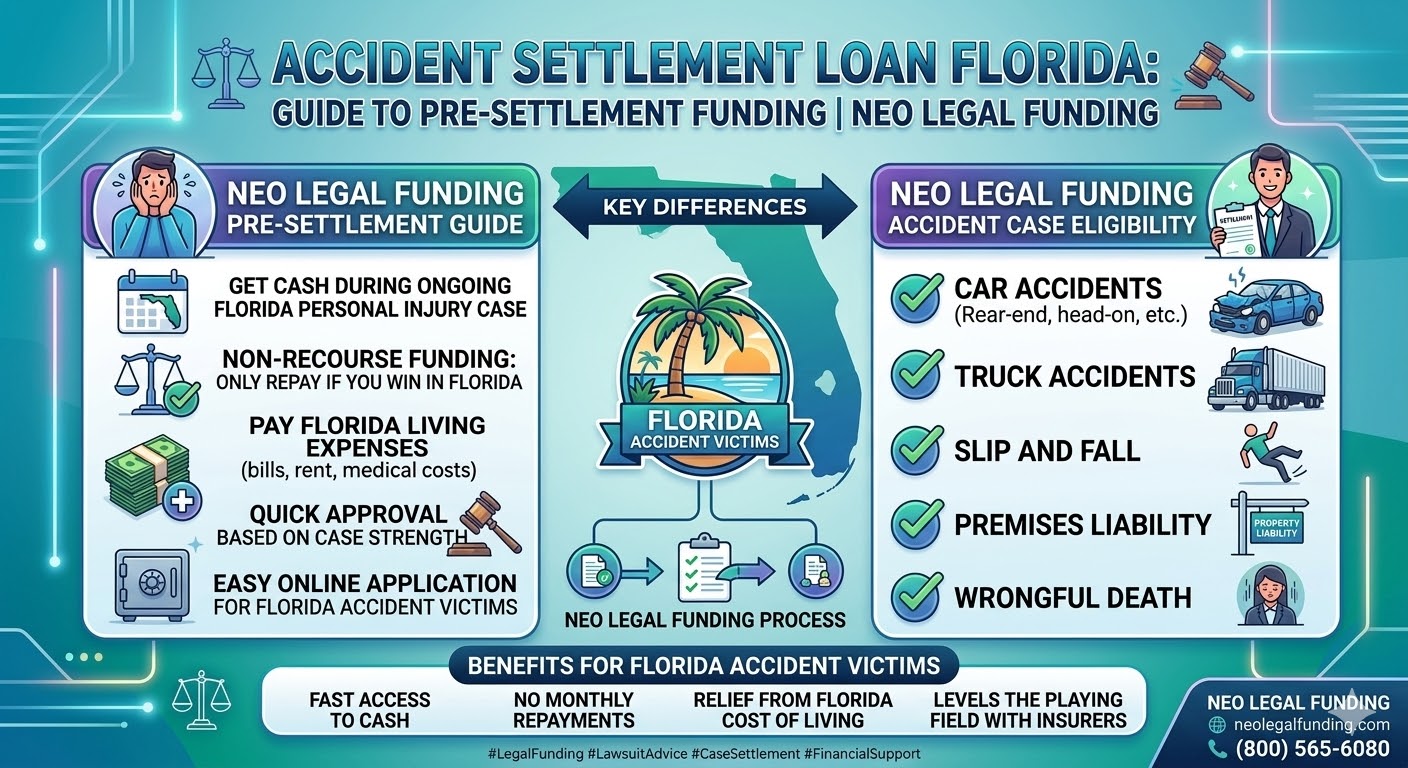

An accident settlement loan is a type of pre-settlement funding that provides cash to plaintiffs involved in personal injury lawsuits while they await the outcome of their case. Unlike traditional loans, this funding is non-recourse, meaning you don’t need to repay the loan unless you win your case. If you lose, you owe nothing. The funding is typically based on the strength of your case, not your credit score or income. This makes it especially helpful for individuals who need immediate financial relief but don’t have access to traditional loans.

3. How Pre-Settlement Funding Works in Florida

The process of securing an accident settlement loan in Florida is straightforward:

File a personal injury claim: Your lawsuit must be active and your attorney must be involved.

Work with your attorney: Your attorney will play a key role in helping you secure pre-settlement funding, as most lenders will only work with cases that are represented by a licensed attorney.

Case evaluation: The funding company will review the merits of your case. They’ll consider factors such as the severity of your injuries and the likelihood of winning the case.

Approval and funding: Once approved, you’ll receive the loan, typically within 24–48 hours. The funds can be used for living expenses, medical bills, or anything else you need while waiting for your settlement.

This is particularly useful in Florida, where personal injury cases, especially those involving car accidents, can take months or even years to resolve.

4. Who Qualifies for an Accident Settlement Loan in Florida?

To qualify for an accident settlement loan in Florida, certain criteria must be met:

Active legal case: You must have an ongoing personal injury lawsuit.

Representation by an attorney: The loan provider will typically only approve loans for cases that are represented by a licensed attorney.

Strong case: Lenders assess the strength of your case based on factors like liability, potential damages, and how likely it is to result in a favorable outcome.

Case type: Common qualifying cases include auto accidents, slip and fall injuries, medical malpractice, and wrongful death.

Because the loan is non-recourse, your credit score and income are not factors in the approval process.

5. Common Personal Injury Cases That Qualify

In Florida, various types of personal injury cases are eligible for pre-settlement funding:

Auto accidents: Car, truck, and motorcycle accidents are common cases where plaintiffs seek accident settlement loans.

Workplace injuries: Accidents at work leading to injuries that are being disputed.

Slip and fall: Injuries caused by negligence on someone else’s property.

Medical malpractice: Lawsuits involving injuries from medical negligence.

Wrongful death: Families seeking justice and compensation for a loved one’s death due to someone else’s negligence.

If you have a case in one of these areas, you could be eligible for a settlement loan in Florida.

6. Financial Benefits of Getting an Accident Settlement Loan

Accident settlement loans provide immediate financial relief during the waiting period of your lawsuit. This can help cover:

Medical bills: Get your treatments covered while you await compensation.

Living expenses: Pay for daily necessities like rent, groceries, and utilities without worrying about falling behind.

No need to accept lowball offers: Settlement loans allow you to hold out for the fair settlement you deserve instead of accepting an early, lower settlement offer due to financial pressure.

The financial benefits are clear, especially in high-cost states like Florida, where medical and living expenses can add up quickly.

7. Cost & Fees: What to Expect

The cost of accident settlement loans can vary widely depending on the lender and the specifics of your case. Typically, fees are a percentage of your loan, which is taken from your settlement if you win the case. Be sure to discuss all potential fees with your lawyer before applying for a loan.

Interest rates: The rates can be steep—sometimes 2%–4% per month, which means they can add up quickly if your case takes a long time.

Repayment: Since settlement loans are non-recourse, repayment is only required if you win your case. If you lose, you don’t owe anything.

Always ask for transparency regarding the total amount you will owe, and ensure you understand the terms before accepting a loan.

8. Risks & Disadvantages

While accident settlement loans can provide much-needed financial relief, they come with risks:

High fees: The longer your case takes to settle, the more expensive the loan can become.

Reduced settlement: The loan and its fees will be deducted from your final settlement, potentially leaving you with a smaller payout.

Not guaranteed: If your case is lost, you don’t owe anything, but not all personal injury cases are successful.

It’s essential to carefully evaluate the costs and risks before deciding if an accident settlement loan is right for you.

9. How to Compare Pre-Settlement Funding Companies

When choosing a provider for your accident settlement loan, consider the following factors:

Funding speed: Look for lenders that offer fast disbursements (24–48 hours).

Non-recourse funding: Ensure the lender offers non-recourse loans, meaning you only repay if you win.

Rates and fees: Compare interest rates and ensure the terms are transparent. Some companies have lower rates but hidden fees.

Reputation: Check for client reviews, BBB ratings, and the provider’s track record. The best companies will have positive feedback and a solid reputation for reliability and transparency.

10. Tips Before Applying for a Settlement Loan

Before applying for a pre-settlement loan, follow these tips:

Consult with your attorney: Your attorney is a vital part of the process and should help guide your decision.

Understand your case value: Know the potential value of your settlement to avoid borrowing more than necessary.

Read the contract thoroughly: Always review the terms of the loan carefully with your attorney before signing anything.

Compare providers: Don’t settle for the first offer. Shop around and compare terms from multiple providers to get the best deal.

11. Frequently Asked Questions

Are settlement loans worth it?

For many, settlement loans are a useful financial tool to bridge the gap during long litigation periods. However, they can be expensive, so make sure the benefits outweigh the costs in your situation.

How long does approval take in Florida?

Approval for pre-settlement funding typically takes 24–48 hours after your case is evaluated.

Do settlement loans affect my credit score?

No. Since settlement loans are non-recourse, they do not require a credit check and do not affect your credit score.

Can I apply more than once?

Yes, in some cases, you can apply for additional funding if your case takes longer than expected. However, this depends on the lender’s policies and your current loan balance.

12. Conclusion

Accident settlement loans in Florida provide an invaluable resource for those struggling financially during a lawsuit. If you need immediate funds for medical bills, living expenses, or other costs, pre-settlement funding can be a solution. However, it’s crucial to weigh the benefits against the costs and risks, and always consult with your attorney before making any decisions. Ready to get started? Contact us at Neo Legal Funding for a free evaluation today!

About the Author

Neo Legal Funding Team specializes in providing pre-settlement funding solutions

for individuals involved in auto accident and personal injury claims across the United States.

The team works closely with plaintiffs and attorneys to help clients explore financial options

while their cases are still pending.

With experience in legal funding processes and claim evaluation, Neo Legal Funding focuses on

helping clients understand how funding works, what to expect, and how to make informed decisions.

Last Updated: April 2026